Welcoming a new baby into your family is one of life’s most joyful experiences—but it also comes with significant financial considerations. Between taking time off work, managing medical bills, and adjusting to new expenses, many New Jersey parents feel overwhelmed by the financial side of having a baby.

The good news? New Jersey offers some of the most generous parental leave benefits in the country, and there are smart strategies to maximize the money available to both moms and dads. Additionally, baby hospital indemnity insurance can provide an extra financial cushion that many families don’t even know exists.

This comprehensive guide will walk you through everything you need to know about New Jersey’s parental leave programs, how to get the most money possible for your family, options for self-employed parents, and how baby hospital indemnity insurance works. Whether you’re planning ahead or your baby is already on the way, understanding these benefits can put thousands of extra dollars in your pocket when you need it most.

Have questions or need personalized guidance? Contact Binyomin Terebelo at (551) 238-7791 for expert assistance navigating your parental leave and insurance options.

Understanding New Jersey’s Parental Leave Benefits: The Basics

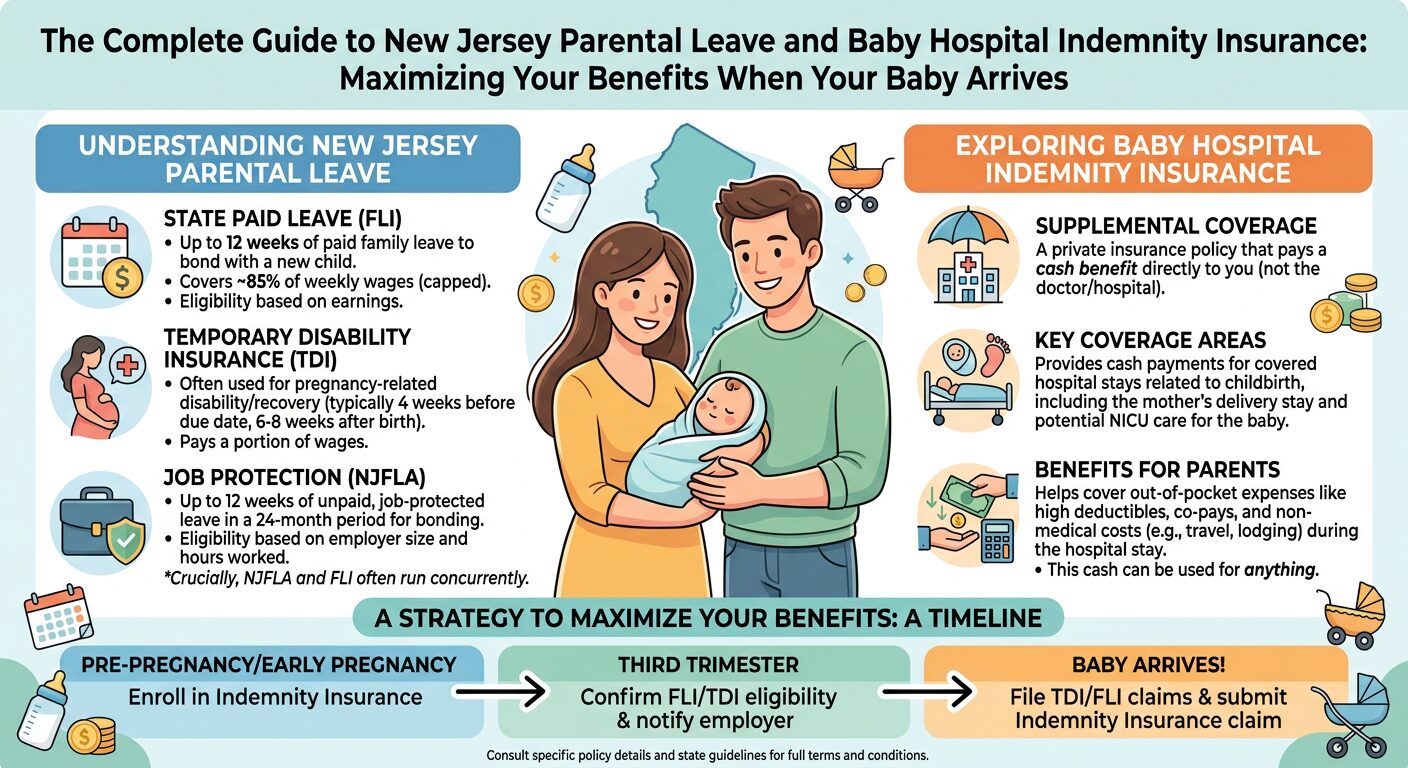

New Jersey operates two separate but complementary programs that provide paid leave for new parents:

1. Temporary Disability Insurance (TDI)

This program provides benefits to mothers for the physical recovery period after childbirth. Think of this as medical leave—it covers the time when mom is physically recovering from pregnancy and delivery.

2. Family Leave Insurance (FLI)

This program provides benefits for bonding with a new baby and is available to both mothers and fathers. This is the time you spend getting to know your baby, adjusting to parenthood, and establishing your new family routine.

The beauty of New Jersey’s system is that mothers can receive BOTH types of benefits, while fathers can receive FLI benefits. When coordinated properly, this means your family can have paid parental leave coverage for several months.

New Jersey Family Leave Insurance (FLI): What You Need to Know

How Much Money Can You Receive?

As of 2025, New Jersey’s Family Leave Insurance pays 85% of your average weekly wage, up to a maximum of $1,081 per week. This is one of the highest benefit rates in the nation.

Here’s what this means in real numbers:

- If you earn $1,200 per week, you’ll receive $1,020 per week (85% of your wage)

- If you earn $1,500 per week, you’ll receive the maximum of $1,081 per week

- If you earn $800 per week, you’ll receive $680 per week (85% of your wage)

Over a full 12-week leave period, this can amount to nearly $13,000 in benefits—money that goes directly to you to use however you need.

How Long Can You Take Leave?

New Jersey FLI provides 12 weeks of paid leave within your baby’s first year. You have two options for how to use this time:

Option 1: Consecutive Leave

Take all 12 weeks in a row (84 consecutive days). This is the traditional approach—you take your full leave period immediately after your baby arrives.

Option 2: Intermittent Leave

Take up to 56 individual days spread throughout your baby’s first year. This flexible option allows you to return to work part-time or take leave in chunks as needed.

Who Is Eligible?

To qualify for New Jersey FLI, you must have:

- Worked in New Jersey and had FLI contributions deducted from your paycheck (you’ll see this as a small percentage on your pay stub)

- Earned at least $260 per week for 20 weeks, OR earned a total of $13,000 during your base year (the 52 weeks before you file your claim, not including the most recent 8 weeks)

Most employees in New Jersey automatically have FLI contributions deducted from their paychecks, so if you’ve been working in the state, you’re likely already covered.

For Mothers: Combining Temporary Disability and Family Leave Insurance

Mothers have access to a powerful combination of benefits that can provide paid leave for several months:

Phase 1: Temporary Disability Insurance (TDI) for Recovery

Before you can bond with your baby, you need to recover from childbirth. New Jersey’s TDI program provides benefits during this medical recovery period.

How long does TDI last?

- Vaginal delivery: Typically 4 weeks of benefits (starting from your delivery date)

- C-section delivery: Typically 6 weeks of benefits (starting from your delivery date)

- Complications: Additional time may be approved with doctor’s documentation

How much does TDI pay?

TDI also pays 85% of your average weekly wage, up to the same $1,081 weekly maximum.

Important note: If you experience pregnancy complications before delivery (such as bed rest ordered by your doctor), you may be eligible for TDI benefits even before your baby arrives.

Phase 2: Family Leave Insurance (FLI) for Bonding

After your TDI recovery period ends, you transition to FLI benefits for bonding with your baby. This gives you an additional 12 weeks of paid leave.

The Timeline for Mothers:

- Weeks 1-4 (or 1-6): Receive TDI benefits for physical recovery

- Weeks 5-16 (or 7-18): Receive FLI benefits for bonding with baby

- Total paid leave: 16-18 weeks depending on delivery type

This means mothers can receive four to four-and-a-half months of paid leave when combining both programs.

How to Apply as a Mother

For TDI Benefits:

Your doctor will complete paperwork certifying your disability due to pregnancy and childbirth. You’ll submit this claim either:

- Through the state plan (if your employer uses the state system)

- Through your employer’s private plan (some employers use private insurance carriers)

For FLI Benefits:

If you received TDI through the state plan, New Jersey will automatically mail you a New Mother Bonding Notice (Form FL-2) when your TDI benefits are ending. This form makes it easy to transition to FLI benefits—simply complete and return it.

If you received TDI through a private plan or didn’t receive TDI at all, you’ll need to submit a new FLI application online at myleavebenefits.nj.gov.

For Fathers: Accessing Your Family Leave Benefits

Fathers are fully eligible for the 12 weeks of Family Leave Insurance to bond with their new baby. Unfortunately, many dads don’t realize they have this benefit or don’t take advantage of it. This is money you’ve already paid into through payroll deductions—you’ve earned this benefit!

How Much Can Fathers Receive?

Fathers receive the same benefit rate as mothers: **85% of average weekly wage, up to $1,081 per week, for up to 12 weeks**. That’s potentially nearly $13,000 in benefits.

When Can Fathers Take Leave?

Fathers can take their 12 weeks of FLI anytime within the baby’s first year. This flexibility allows families to strategize:

Strategy 1: Overlap with Mom

Dad takes leave at the same time as mom, providing maximum family support during the early weeks.

Strategy 2: Sequential Leave

Dad takes leave after mom returns to work, extending the total time a parent is home with the baby.

Strategy 3: Intermittent Leave

Dad uses the 56-day intermittent option to be home on specific days throughout the first year—perhaps taking Fridays off for several months, or being home one week per month.

How to Apply as a Father

Fathers apply for FLI benefits online at myleavebenefits.nj.gov. You’ll need:

- Your baby’s birth certificate

- Information about your employment and wages

- Your bank account information for direct deposit

The application process is straightforward and can typically be completed in 15-20 minutes.

Maximizing Parental Leave Money: Smart Strategies for New Jersey Families

Now that you understand the basics, let’s talk about strategies to maximize the money your family receives:

Strategy #1: Plan Your Timing Strategically

For Maximum Total Family Leave:

Have mom take her full TDI recovery period (4-6 weeks) plus her full 12 weeks of FLI consecutively. Then have dad take his full 12 weeks of FLI immediately after mom returns to work.

Result: Your family has a parent home with baby for 28-30 weeks (about 7 months) with paid benefits.

For Maximum Flexibility:

Have mom take her TDI and some FLI consecutively, while dad uses the intermittent 56-day option throughout the first year to provide ongoing support.

Result: Mom gets extended bonding time, while dad can be present for important moments, appointments, and challenging days throughout the entire first year.

Strategy #2: Understand the Tax Implications

New Jersey FLI and TDI benefits are subject to federal income tax but are NOT subject to New Jersey state income tax. This means:

- You’ll receive the full benefit amount in your payments

- You’ll need to report these benefits on your federal tax return

- You may want to set aside approximately 10-15% for federal taxes, depending on your tax bracket

- Consider adjusting your W-4 withholding at work to account for this additional income

Pro tip: You can request voluntary federal tax withholding from your benefit payments to avoid a surprise tax bill. Contact the Division of Temporary Disability and Family Leave Insurance to set this up.

Strategy #3: Coordinate with Employer Benefits

Some New Jersey employers offer additional paid parental leave beyond the state programs. Check your employee handbook or speak with HR to understand:

- Does your employer offer paid parental leave?

- Can you use employer leave in addition to state benefits, or must you use state benefits first?

- Does your employer “top up” state benefits to bring you to 100% of your salary?

If your employer offers additional benefits, you may be able to extend your paid leave even further or receive your full salary during leave.

Strategy #4: Use the Intermittent Option Wisely

The 56-day intermittent option is incredibly valuable but often underutilized. Consider using it for:

- Gradual return to work: Take 2-3 days per week off for the first month back, easing the transition

- Daycare transition: Be home on certain days as your baby adjusts to childcare

- Appointment days: Use leave days for pediatrician visits, vaccinations, and other appointments

- Challenging periods: Save some days for sleep regressions, teething, or illness

- Special moments: Be present for first holidays, milestones, or family events

Strategy #5: Apply Promptly and Follow Up

Benefits are typically paid within 2-3 weeks of filing a complete claim, but delays can occur. To maximize your money:

- Apply as soon as you’re eligible (don’t wait)

- Ensure all paperwork is complete and accurate

- Respond immediately to any requests for additional information

- Follow up if you don’t receive payment within 3 weeks

- Set up direct deposit for fastest payment

Strategy #6: Consider Supplemental Insurance

This brings us to an important additional resource: baby hospital indemnity insurance, which we’ll cover in detail below. This type of insurance can provide thousands of dollars in additional benefits that complement your parental leave income.

Parental Leave for Self-Employed Parents: Yes, You Can Get Benefits Too!

If you’re self-employed, you might think parental leave benefits aren’t available to you. Good news: self-employed individuals in New Jersey CAN participate in the state’s TDI and FLI programs—but you need to opt in.

How Self-Employed Coverage Works

Unlike employees who automatically have contributions deducted from paychecks, self-employed individuals must voluntarily elect coverage and pay contributions directly to the state.

Enrolling in Coverage

To participate as a self-employed person:

- Register with the New Jersey Division of Temporary Disability and Family Leave Insurance

- Complete the Application for Voluntary Coverage (Form DS-10)

- This can be done online at myleavebenefits.nj.gov

- Pay Your Contributions

- For 2025, the contribution rate is 0.33% of your income for FLI

- TDI contributions are additional (rates vary)

- Contributions are based on your self-employment income up to $165,800

- You’ll pay quarterly, similar to estimated tax payments

- Maintain Coverage

- You must maintain coverage for at least 12 months before you can claim benefits

- Continue paying contributions to keep coverage active

Planning Ahead Is Essential

This is crucial: If you’re self-employed and planning to have a baby, you need to enroll in coverage BEFORE you become pregnant. You cannot enroll once you’re already pregnant and expect to receive benefits for that pregnancy.

Timeline for self-employed parents:

- Enroll in TDI/FLI coverage at least 12 months before you plan to have a baby

- Pay your quarterly contributions consistently

- When your baby arrives, you’ll be eligible for the same benefits as employees

Benefits for Self-Employed Parents

Once you’re covered, you receive the same benefits as employees:

- Mothers: TDI for recovery (4-6 weeks) plus FLI for bonding (12 weeks)

- Fathers: FLI for bonding (12 weeks)

- Benefit amount: 85% of your average weekly self-employment income, up to $1,081/week

Cost-Benefit Analysis for Self-Employed

Let’s look at whether this makes financial sense:

Example: Self-employed parent earning $75,000 annually

- Annual FLI contribution: $247.50 (0.33% of $75,000)

- Annual TDI contribution: Approximately $300-400

- Total annual cost: About $550-650

Potential benefit received:

- 12 weeks of FLI: Up to $12,972

- Plus TDI for mothers: Additional 4-6 weeks

Return on investment: Even after paying contributions for 12 months before claiming, you receive far more in benefits than you paid in contributions.

Special Considerations for Business Owners

If you own a business with employees:

- You may already be required to provide TDI/FLI coverage for your employees

- You can elect to cover yourself under your business’s plan

- Consult with your business insurance broker or benefits administrator

- This may be simpler than enrolling individually

What If You Don’t Have Coverage?

If you’re self-employed and didn’t enroll in advance, you won’t be eligible for state TDI/FLI benefits for your current pregnancy. However, you still have options:

- Enroll now for future pregnancies or for your partner’s future pregnancies

- Consider private disability insurance that covers maternity (though this also requires enrollment before pregnancy)

- Explore baby hospital indemnity insurance (covered below) which can provide cash benefits for hospital stays

- Look into business interruption insurance that may provide some income replacement

For personalized guidance on self-employed parental leave options, contact Binyomin Terebelo at (551) 238-7791.

Baby Hospital Indemnity Insurance: An Extra Financial Safety Net

Now let’s talk about a benefit that many new parents don’t know exists but can provide significant financial relief: baby hospital indemnity insurance.

What Is Hospital Indemnity Insurance?

Hospital indemnity insurance is a type of supplemental insurance that pays YOU cash benefits when you or your baby are admitted to the hospital. Unlike your regular health insurance, which pays your doctors and hospital directly for medical care, hospital indemnity insurance pays money directly to you to use however you need.

Think of it this way:

- Your health insurance pays for medical care (doctor fees, hospital charges, medications)

- Hospital indemnity insurance pays you cash to help with all the OTHER expenses that come with a hospital stay

How Is This Different from Regular Health Insurance?

This is an important distinction that confuses many people:

Your Regular Health Insurance:

- Pays medical providers for medical services

- Subject to deductibles, copays, and coinsurance

- You may still owe thousands in out-of-pocket costs

- Doesn’t help with non-medical expenses

Hospital Indemnity Insurance:

- Pays YOU directly, regardless of what your health insurance pays

- Fixed benefit amounts (not based on actual medical costs)

- You can use the money for anything—medical bills, rent, groceries, childcare, lost wages

- Works alongside your health insurance, not instead of it

How Hospital Indemnity Insurance Works for Childbirth

When you have a baby, hospital indemnity insurance typically provides:

1. Hospital Admission Benefit

A lump sum payment when you’re admitted to the hospital for delivery. Common amounts range from $1,000 to $2,000.

2. Daily Hospital Stay Benefit

A payment for each day you remain in the hospital. Common amounts range from $200 to $500 per day.

3. Newborn Benefit

Separate benefits for your baby’s hospital stay, including:

- Admission benefit for the baby

- Daily benefits for each day the baby is hospitalized

- Coverage for NICU stays if needed (often at higher daily rates)

Real-World Example: How Much Money Can You Receive?

Let’s look at a typical scenario with a common hospital indemnity plan:

Mom’s Benefits:

- Hospital admission: $1,200

- 2-day hospital stay: $400 ($200/day × 2 days)

- Mom’s total: $1,600

Baby’s Benefits:

- Newborn admission: $1,200

- 2-day hospital stay: $400 ($200/day × 2 days)

- Baby’s total: $1,600

Total family benefit: $3,200

And this is for an uncomplicated vaginal delivery with a short stay. If you have a C-section (longer hospital stay) or if your baby needs NICU care, the benefits can be substantially higher. Enhanced or higher-tier hospital indemnity plans can provide up to $15,000 in total benefits—potentially $5,000 to $10,000 or more for standard plans, with premium plans reaching that $15,000 lump sum threshold.

What Can You Use This Money For?

The beauty of hospital indemnity insurance is that you can use the money for ANYTHING. Common uses include:

Medical Expenses:

- Meeting your health insurance deductible

- Paying copays and coinsurance

- Covering costs for services not covered by insurance

- Paying for private room upgrades or other comfort items

Non-Medical Expenses:

- Replacing lost income if you take unpaid leave

- Covering rent or mortgage while you’re not working

- Paying for childcare for older children

- Buying baby supplies and equipment

- Covering increased food and household expenses

- Paying for help around the house during recovery

- Transportation costs to and from the hospital

- Parking fees during hospital stays

When Should You Enroll in Hospital Indemnity Insurance?

Timing is critical. Most hospital indemnity plans have waiting periods or limitations for maternity coverage. Here’s what you need to know:

Best Time to Enroll: BEFORE You’re Pregnant

Many plans require you to be enrolled for 10-12 months before maternity benefits are available. If you’re planning to have a baby in the next year or two, enroll now.

Can You Enroll During Pregnancy?

Some plans allow enrollment during pregnancy, but benefits may be limited or subject to waiting periods. Check specific plan terms.

Open Enrollment Periods:

If you get insurance through your employer, you can typically enroll in hospital indemnity insurance during:

- Your company’s annual open enrollment period

- Within 30 days of a qualifying life event (marriage, birth of a child, etc.)

Individual Plans:

If you’re purchasing an individual plan (not through an employer), you can typically apply anytime, but maternity waiting periods will apply.

How Much Does Hospital Indemnity Insurance Cost?

Hospital indemnity insurance is generally affordable, especially compared to the potential benefits. Typical costs:

Through an Employer:

- Individual coverage: $15-40 per month

- Family coverage: $30-80 per month

Individual Plans:

- Individual coverage: $30-75 per month

- Family coverage: $60-150 per month

Cost-Benefit Analysis:

Even if you pay $50/month for 12 months ($600 total) before having a baby, and then receive $3,200 in benefits, you’ve gained $2,600—and you still have the coverage for future hospitalizations.

Important Things to Know About Hospital Indemnity Insurance

1. It’s Not Comprehensive Health Insurance

Hospital indemnity insurance is supplemental coverage. You still need regular health insurance for medical care. This is extra protection on top of your health insurance.

2. Coverage Continues Beyond Childbirth

Once you have hospital indemnity insurance, it covers you for ANY hospital admission—not just childbirth. This includes:

- Accidents and injuries

- Illnesses requiring hospitalization

- Surgeries

- Your children’s hospital stays

3. Pre-Existing Condition Limitations

Some plans may have limitations for pre-existing conditions. Read the policy carefully.

4. NICU Coverage Can Be Substantial

If your baby requires NICU care, hospital indemnity benefits can be significant. NICU stays often qualify for higher daily benefit amounts and can last for weeks or months.

5. Both Parents Can Have Coverage

If both parents have hospital indemnity insurance through their respective employers, you may be able to claim benefits from both policies—potentially doubling your benefits.

Questions to Ask When Choosing a Hospital Indemnity Plan

Before enrolling, ask:

- What is the maternity waiting period? (How long must you be covered before maternity benefits are available?)

- What are the specific benefit amounts?

- Hospital admission benefit

- Daily hospital stay benefit

- Newborn admission benefit

- Newborn daily benefit

- NICU daily benefit

- Are there any benefit maximums? (Some plans cap total annual benefits)

- Does the plan cover both vaginal delivery and C-section? (Most do, but confirm)

- How are benefits paid? (Direct deposit, check, how quickly?)

- Can benefits be assigned to providers? (Or do they only pay you directly?)

- What other hospitalizations are covered? (Understand your full coverage)

Combining Hospital Indemnity Insurance with Parental Leave Benefits

Here’s where things get really powerful: when you combine New Jersey’s generous parental leave benefits with hospital indemnity insurance, you create a comprehensive financial safety net for your growing family.

The Complete Financial Picture:

Mom’s Income:

- TDI benefits: 4-6 weeks at 85% of salary

- FLI benefits: 12 weeks at 85% of salary

- Hospital indemnity: $1,600+ lump sum

- Total: 16-18 weeks of paid leave plus cash benefit

Dad’s Income:

- FLI benefits: 12 weeks at 85% of salary

- Hospital indemnity (if covered): $1,600+ lump sum

- Total: 12 weeks of paid leave plus cash benefit

Combined Family Benefits:

- 28-30 weeks of paid parental leave (if taken sequentially)

- $3,200+ in hospital indemnity benefits

- Potential for additional employer-provided benefits

This combination can provide tens of thousands of dollars in income replacement and cash benefits during your baby’s first year.

Taking Action: Your Step-by-Step Checklist

Ready to maximize your parental leave and insurance benefits? Here’s your action plan:

If You’re Planning to Have a Baby (Not Yet Pregnant):

☐ Step 1: Verify you’re covered by New Jersey TDI/FLI

- Check your pay stub for deductions

- If self-employed, enroll in voluntary coverage NOW

☐ Step 2: Enroll in hospital indemnity insurance

- Check if your employer offers it during open enrollment

- If not, research individual plans

- Enroll at least 10-12 months before trying to conceive

☐ Step 3: Review your employer’s parental leave policies

- Understand what additional benefits may be available

- Learn how employer leave coordinates with state benefits

☐ Step 4: Calculate your potential benefits

- Estimate your TDI/FLI benefit amounts based on your salary

- Understand your hospital indemnity benefit amounts

- Create a budget for your leave period

☐ Step 5: Start saving

- Even with generous benefits, you’ll likely have some income reduction

- Build an emergency fund to cover the gap

If You’re Currently Pregnant:

☐ Step 1: Confirm your TDI/FLI coverage

- Contact your employer’s HR department

- Understand whether you’re on state plan or private plan

☐ Step 2: Check hospital indemnity insurance options

- See if you can still enroll (some plans allow it)

- Understand any limitations for current pregnancy

☐ Step 3: Gather required documentation

- Get forms from your doctor

- Collect employment and wage information

- Set up online account at myleavebenefits.nj.gov

☐ Step 4: Plan your leave strategy

- Decide whether to take consecutive or intermittent leave

- Coordinate timing with your partner

- Communicate plans with your employer

☐ Step 5: Prepare your TDI application

- Your doctor will complete medical certification

- Be ready to file as soon as you go on leave

After Your Baby Arrives:

☐ Step 1: File your TDI claim (for mothers)

- Submit within 30 days of going on leave

- Include all required documentation

☐ Step 2: File your hospital indemnity claim

- Submit hospital admission paperwork

- Include baby’s birth certificate

- Follow up to ensure payment

☐ Step 3: Watch for your New Mother Bonding Notice (FL-2)

- If you received state plan TDI, this will arrive automatically

- Complete and return promptly to transition to FLI

☐ Step 4: File FLI claim (for fathers and mothers not receiving TDI)

- Apply online at myleavebenefits.nj.gov

- Include baby’s birth certificate

- Provide employment and wage information

☐ Step 5: Set up direct deposit

- Ensures fastest payment of benefits

- Reduces risk of lost checks

☐ Step 6: Track your benefits

- Keep records of all payments received

- Note any issues or delays

- Follow up on missing payments

Common Questions and Concerns

Q: Will taking parental leave affect my job security?

A: New Jersey law provides job protection for employees taking family leave. Under the New Jersey Family Leave Act (NJFLA), eligible employees can take up to 12 weeks of job-protected leave. You must be returned to your same position or an equivalent position when you return. However, job protection requirements vary based on employer size, so check your specific situation.

Q: Can both parents take leave at the same time?

A: Yes! Both parents can take FLI simultaneously if desired. This can provide maximum family support during the early weeks.

Q: What if I want to take more than 12 weeks?

A: You can take additional unpaid leave under NJFLA (up to 12 weeks total in a 24-month period). Some employers also offer additional paid or unpaid leave. After exhausting these options, you may be able to use FMLA (federal Family and Medical Leave Act) for additional unpaid, job-protected leave.

Q: Do I have to take all 12 weeks consecutively?

A: No. You can use the intermittent option (56 individual days) for maximum flexibility.

Q: Will my health insurance continue during leave?

A: Generally yes. Your employer must continue your health insurance during job-protected leave, though you may need to continue paying your portion of premiums.

Q: What if my employer doesn’t approve my leave?

A: If you’re eligible under state law, your employer cannot deny your leave. If you encounter problems, contact the New Jersey Department of Labor.

Q: Can I work part-time while receiving benefits?

A: This is complex and depends on your specific situation. Generally, you cannot work for the employer from whom you’re taking leave while receiving benefits. Consult with the Division of TDI/FLI about your specific circumstances.

Get Expert Help Navigating Your Benefits

Understanding and maximizing parental leave and insurance benefits can be complicated. Every family’s situation is unique, and the rules can be confusing. Don’t leave money on the table or miss out on benefits you’ve earned.

For personalized guidance on:

- Maximizing your New Jersey parental leave benefits

- Enrolling in hospital indemnity insurance

- Coordinating benefits between both parents

- Self-employed coverage options

- Understanding your specific situation

Contact Binyomin Terebelo at (551) 238-7791

Binyomin specializes in helping New Jersey families navigate parental leave benefits and insurance options. He can help you understand exactly what you’re entitled to, how to apply, and strategies to maximize your benefits—ensuring you get every dollar you deserve during this important time.

Conclusion: You’ve Earned These Benefits—Make Sure You Get Them

Having a baby is expensive, and taking time off work adds financial stress to an already overwhelming time. But New Jersey provides some of the best parental leave benefits in the country, and hospital indemnity insurance can provide additional financial support.

The key is understanding what’s available, planning ahead, and taking action to secure your benefits. Whether you’re an employee or self-employed, whether you’re planning ahead or your baby is already on the way, there are steps you can take to maximize the financial support available to your family.

Remember:

- Both parents can receive benefits—don’t leave dad’s benefits unclaimed

- Self-employed parents can participate, but must enroll in advance

- Hospital indemnity insurance provides cash benefits on top of your health insurance

- Strategic planning can extend your family’s paid leave for many months

- Expert guidance can help you navigate the system and maximize your benefits

Your baby’s first year is precious. These benefits exist to help you focus on your family instead of worrying about finances. Take advantage of everything available to you—you’ve earned it.

Ready to get started? Call Binyomin Terebelo at (551) 238-7791 for personalized assistance with your parental leave and insurance benefits.

Disclaimer: This article provides general information about New Jersey parental leave benefits and hospital indemnity insurance. Specific benefit amounts, eligibility requirements, and coverage details may vary based on individual circumstances, employer policies, and insurance plans. Always verify current information with the New Jersey Division of Temporary Disability and Family Leave Insurance, your employer, and your insurance provider. This article is not legal or financial advice.